Technology

What is Blockchain?

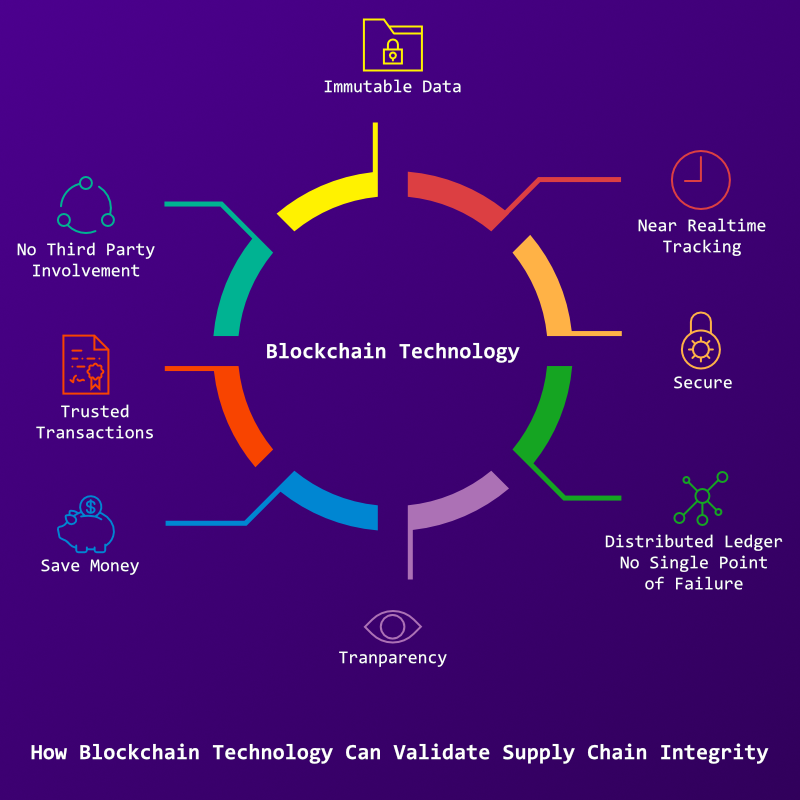

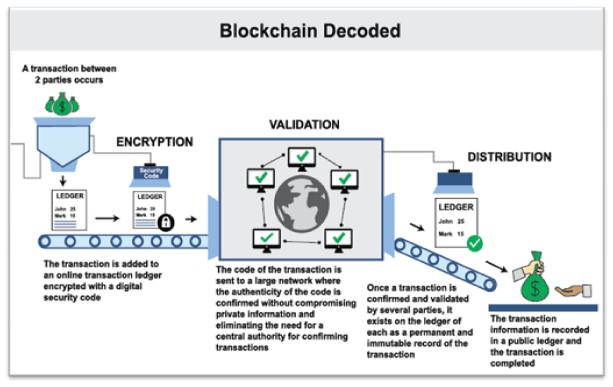

A Blockchain is a digital, immutable, distributed ledger that chronologically records transactions in near real time. The prerequisite for each subsequent transaction to be added to the ledger is the respective consensus of the network participants (called nodes), thereby creating a continuous mechanism of control regarding manipulation, errors, and data quality.

The Lure of blockchain was its method of verifying and tracking transactions. Instead of a trusted third-party or a central bank, it relies on consensus among a peer-to-peer network of computers based on complex algorithms.

Anatomy of the Blockchain architecture

The blockchain architecture consists of a few fundamental concepts like decentralization, digital signature, mining and data integrity.

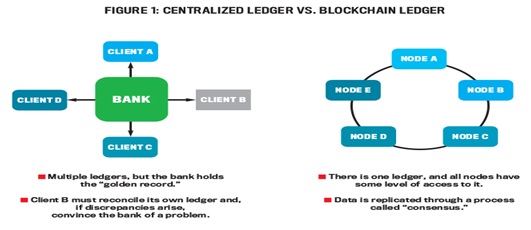

- Decentralization:Block chain explicitly distributes control amongst all peers in the transaction chain.

- Digital signature:Blockchain enables an exchange of transactional value using public keys by the mechanism of a unique digital sign.

- Data integrity:Complex algorithms and agreement among users ensures that transaction data, once agreed upon, cannot be tampered . Data stored on blockchain acts as a single version of truth for all parties involved hence reducing the risk of fraud.

What is Distributed Ledger ?

A distributed ledger can be described as a ledger of any transactions or contracts maintained in decentralized form across different locations and people, eliminating the need for a central authority to keep a check against manipulation. All the information on it is securely and accurately stored using cryptography and can be accessed using keys and cryptographic signatures.

The reason why the blockchain has gained so much admiration is that:

- It is decentralized.

- Risk reduction

- It is immutable,

- It is transparent

- Reduction of

- settlement time.

- Material cost reduction.

- Elimination of error.

Determine the nature of blockchain implementation

Open vs Permissioned Permissioned

blockchains (Private block chain)

A type of block chain which allow a mixed bag between the public and private blockchains with lots of customization options. Such blockchains are built such that they grant special permissions to each participant for specific functions to be performed—like read, access and write information.

Open blockchain

A public blockchain network is completely open and anyone is free to join and participate in the core activities of the blockchain network. It helps maintain its self-governed nature.

Understanding relevance of Block chain in banking

Block chain is being widely debated and has become the new buzz word for multiple industries, especially banking. Banks across the country have successfully initiated collaboration with specialized firms (Fintech) and/or consulting firms to build proof-of-concepts . This implies the seriousness of banks towards the Blockchain technology and its eagerness to understand how Blockchain can address and resolve few pain points in the current state process.Because blockchain introduces a decentralized ledger, it stores a bank’s complete transaction history across dozens, of controlled-access computers replicating a breadcrumb trail of banking activity that is impossible to delete or change. Blockchain reimagines many of the core workflows in finance and banking, from records keeping and cybersecurity to currency, debt and equity management. Blockchain technology possesses all the attractive characteristics needed by a reliable technology involving money matters. It is safe, secure, decentralized, transparent.as.well.as.relatively.cheaper.

Blockchain provides a very high level of safety and security when it comes to exchanging data, information, and money. It also allows users to take advantage of the transparent network infrastructure along with low operational costs with the aid of decentralization. Together, blockchain and banking offer one of the most exciting commercial frontiers of the century.

AREAS IN WHICH BLOCKCHAIN IS CHANGING CURRENT FACE OF BANKING

1. Know-Your-Customer (KYC)

Banks and financial institutions are strictly concerned about the increasing costs that they have to bear in order to comply with AML and KYC i.e. Anti-money Laundering and Know Your Customer norms.

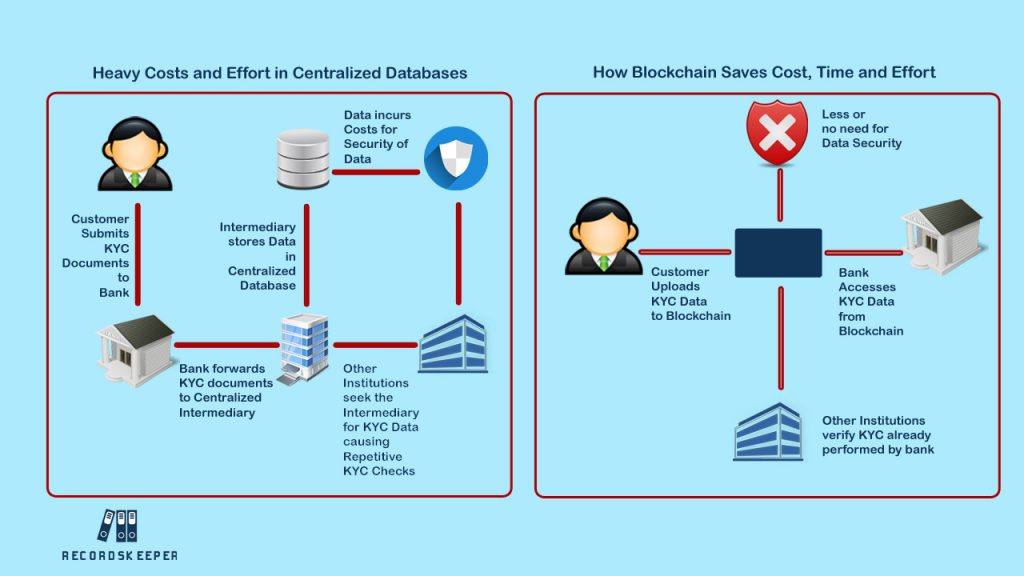

With the adoption of a blockchain system, the independent verification of each client by one bank would be accessible for other banks to use so that the KYC process doesn’t have.to.be.restarted.again.Meaning that the duplication of efforts would be eliminated by the aid of blockchain technology. Moreover, all the updates of clients’ will be to all financial institutions in near real-time. Instead of every bank and third-party vendor maintaining siloed customer data portals, and requiring data duplication with each request, a blockchain system lets authorized users access the same data system. With this system, bank can access details of a customer from any branch. You are assigned a particular customer ID. Whether you open a new account in any other branch of that bank, or close the existing one, detail gets attached to that customer ID.

1. If your account at current branch has all KYC documents linked with it, then you just don’t need to submit them again. Bank Account Portability works well with this.

2. Account number, customer ID remain intact under bank account portability. So, just branch of your account gets changed.

3. Internet banking will work as usual. Your account overview, history etc can be accessed in the same way as it was earlier.

4. If you have changed your residence address, then you need to prove proofs of new address. This is mandatory.

5. Conversion of NRE account to a Savings account wants you to follow the same procedure.

6. To shift the joint account to new branch, both applicants need to sign the application.. It depends on what criteria your bank has set for the bank account portability.

Current Challenges

Here are some major KYC compliance challenges that banks are facing:

1. Data integration: currently, several third-party data providers and external validation agencies offer data and interfaces to extract the required customer information. However, banks struggle to integrate this data to obtain a consolidated view of the customers, resulting in huge penalties and reputational damage.

2. Expensive technology: post due diligence, banks need to digitize data in the documents to feed it into the repositories. This is an expensive exercise, as it uses advanced technology platforms

3. Evolving regulation: The KYC landscape is constantly facing new regulation across different jurisdictions therefore KYC utilities need to keep updating their guidelines & this increases the need for banks to improve their data collection mechanisms for effective risk management and timely compliance.

4. Fragmented approach: Banks do not have a single, unified KYC system for its various lines of business like wealth management, asset management, and brokerage. Maintaining these puts banks under immense pressure and adds costs.

By uploading your identity to the blockchain, you have full and complete control over yourself. So, how will that help with KYC? Suppose you have to go and open an account in a bank, the bank will simply ask you to give access to your identity instead of a centralized third party.

Secondly, the banks could be part of their own private and permission blockchain networkNow suppose Ram has completed KYC regulations with Bank A, they can then simply upload the details on the blockchain. Since the blockchain is not owned by the central repository, anyone, who is part of the network can upload information and share it with everyone else.Suppose Ram wants to open an account in bank B. Instead of starting the whole compliance process from scratch, they can simply access the blockchain and get the required KYC data.

Current Pain Points

Current Pain Points

Data integration

Intra-bank applications

Expensive technology

Inter-bank applications

Evolving regulation

Centralized blockchain-based KYC

Fragmented approach

Fraud Proof